As we are all aware, in order to stand any chance of

avoiding catastrophic climate change, governments and businesses have committed

themselves to the challenge of Net Zero.

Net Zero is about completely negating the effects of

greenhouse gasses produced by humankind by 2050.

Impressively, in June 2019 the UK became the first major

economy to commit to and set a legally binding target for Net Zero Carbon (NZC)

emissions by 2050 and since then several major cities have set even more

ambitious targets.

However, less impressively, the Governments pendulum swings

backwards and forwards from time to time and it’s “time” that is actually

running out. We all know we could all do

more, and we know we have clients that have lost contracts because they have

not shouted sufficiently loudly about what they have already done.

Statius has for some time been involved with various energy

and climate change related initiatives for instance:

I.

ISO 50001 the energy management standard, first

published in 2011

II.

The Energy Savings and Opportunity Scheme (ESOS)

Regulations which were made mandatory for specific companies in 2014 and

III.

The Streamlined Energy and Carbon Reduction (SECR)

Regulations which were mandatory for some companies in 2019.

But, in order to maintain our position in the marketplace we

now need, and want, to help clients demonstrate that they are pursuing a

rigorous strategy of Net Zero.

What does this mean?

With both ESOS and SECR we have helped clients calculate and,

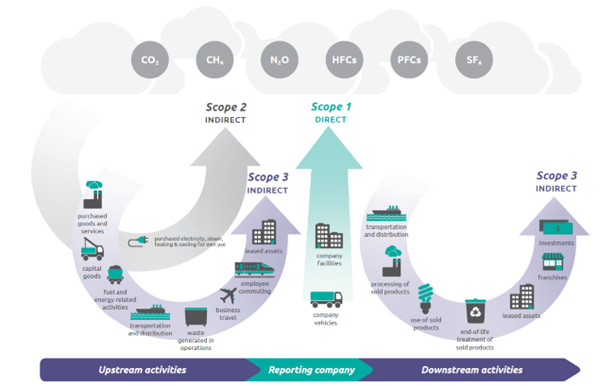

over time reduce, their operational carbon impact. Both regulations concentrate on what are called

Scope 1 & Scope 2 emissions.

Scope 1 are those resulting directly from the day-to-day

operational activities, the running of any production equipment and plant, the

running of transport, vans and cars.

Scope 2 are those resulting from the energy used to

provide heat and power to the facilities you operate.

For larger companies, with sales of over £36m under various

legislation (ESOS & SECR)

you will have already had to track your Scope 1 & 2 carbon emissions for

some years.

However, a far bigger impact results from the emissions that

arise from your external, and out of your direct control, upstream and

downstream operations. These are called

Scope 3 emissions and there are 15 subsections to the type of activity that might

generate these emissions.

Upstream emissions include those arising from:

Purchased goods and services; Capital

goods; Fuel and energy (not in scope 1 & 2); Upstream transportation and

distribution; Waste generated in operations; Business travel; Employee

commuting; Upstream leased assets.

Downstream emissions include those arising from:

Transportation and distribution of sold products; Processing

of sold products; Use of sold products; End of life treatment of sold products;

Downstream leased assets; Franchises; Investments.

Source: Corporate-Value-Chain-Scope 3

Accounting-and reporting Standard (p31)

The different Scope 3 categories are likely to have

different impacts on different companies operating in different sectors. In fact, some categories may not even be

relevant to some companies for instance franchises and investments.

However, if we take a brief, oversimplified, look at some examples:

I.

A manufacturing company is likely to purchase raw

materials and/or components of some kind (Category 1). Each of which will need to be transported to

the company (Category 4) before they are processed by the company on plant and

equipment (Category 2) that will have also been transported to the company

(category 4). During the manufacturing

process waste will inevitably be created (Category 5). Once manufactured or produced goods will then

need to be transported to consumers. (Category 9). If the company is producing something that

uses energy once it is with the end user, anything from lifts, alarm system,

security equipment, laptops, anything to do with heating and cooling (the list

is long), then this energy also needs to be accounted for to (Category 11).

II.

A construction company is likely to have to

purchase, or hire, large items of construction equipment. The carbon emissions from the original manufacture

and then transportation of these items will need to be accounted for (Category

2). Construction companies are also

likely to have a large number of their people or subcontractors working onsite during

the build (Category 7 or possibly category 9, Probably depending on the

contractual relationship). Waste

resulting from the on site operation will also need to be considered (Category

5). The company will also need to

account for emissions resulting from the demolition of the construction works undertaken

(Category 12).

III.

All companies will also need to account for the

emissions resulting from their office operations. This will apply to manufacturing,

construction companies and service companies, for instance; architects,

surveyors, marketing companies or any other professional service provider. All of whom will need to purchase general

office and IT equipment (Category 1). All

companies will also have to account for business travel and employee commuting

(Categories 6 & 7).

Obviously the above are just examples.

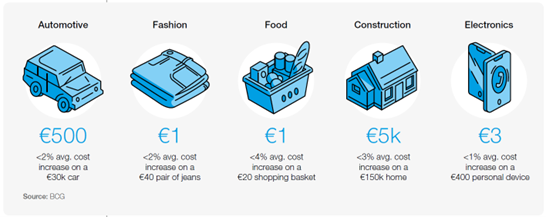

A ray of hope?

If you listen to the news, it might all seem doom and gloom but

there is hope. One report, Net

Zero Challenge: The supply chain opportunity published by the World

Economic Forum (WEF) has a chapter called “Encouraging Economics” in which the

additional costs arising from companies providing Net Zero products and services

are examined.

Overall, because in many products the cost of the raw

materials is only a small part of the cost of the final product, the impact on the

consumers purchase price of the product is actually comparatively small;

according to the study, typically 1-4%. We

have reproduced some examples from the report below:

Source: WEF Net Zero Challenge The Supply

Chain Opportunity 2021 (p21)

Obviously, at the moment with energy prices and the cost-of-living

squeeze (both very topical) things are tight; but as a general principle, would

you be happy to pay the above premiums for products you knew would have a more positive

impact on the planet for the sake of your children and grandchildren? I think I would.

The report also highlights a few case studies and names a

few names. Some examples from companies

you may know include:

o

Ikea, now owns and manages nearly 250,000

hectares of forests which are used to manufacture products locally reducing the

need to transport finished products across the globe

o

Dell, the computer manufacturer, continues to

increase the share of recycled plastics in its products and improving the

repairability and recyclability

o

Merck, the life science company, has developed

several bio-based solvents using renewable and waste materials. Merck have also reduced plastics by 48% and

packaging by 73% in their product lines.

This also reduces transported weight and therefore associated emissions

o

Unilever has developed new dishwasher product

formulations that lead to better cleaning and reduced environmental impacts

Another company (we’d never heard of) Hybrit is focused on

producing emission free steel, so called green steel. Very impressive.

The good news is there is a lot of good stuff NOT reported

in the news… but, we can still do more …

So, what does Net Zero really mean?

At the company level this means that your company has

to determine and account for your carbon emissions across the three sources, or

scopes, of emissions:

o

Scope 1 emissions – direct GHG emissions from

sources controlled and owned by your company

o

Scope 2 emissions – indirect GHG emissions arising

mainly from the purchase of electricity for running your company (IT, heating

and cooling) but also sometimes steam

o

Scope 3 emissions including where relevant, those

arising from each of the 15 categories

The Scope 3 emissions are the most difficult to assess AND

the largest emission set; in fact, Scope 3 emissions often account for more

than 80% of the total emissions produced.

Essentially, it means accounting for the emissions of your entire supply

chain. That’s a huge task. But a necessary one if we are to stand any

chance of getting to Net Zero.

At a lower (product / service) level this is also

given rise to something CIBSE have created

called “TM65

embodied carbon in building services” a document relevant for an enormous

number of companies. TM65 provides a

methodology for doing a lot of sums to calculate the carbon embedded

in anything that is used in a building including; Lifts, security systems, lighting

systems, fire systems, furniture – you name it, if it can be found in a building,

this is the methodology for calculating the embodied carbon.

As can be seen from the diagram below TM65 has a whole set

of modules for which carbon emissions can be calculated.

Source: Embodied carbon in building

services: a calculation methodology. CIBSE (p4)

The structure of TM65, along with something called the global

Product Category Rules (PCRs) allows the calculated carbon emissions to be formulated

into an Environmental Product

Declaration (EPD).

These are a bit like the energy rating you get on a domestic

fridge or a cooker, and they are already available for literally hundreds of

products.

Science based targets

However, as we all know there is a lot of “greenwashing” often

undertaken by companies that are perhaps not as scrupulous as others. As a result, governments, blue chip

organisations and larger clients are now pushing for the adoption of what are

called Science Based Targets. And many of these organisations will want you

to make assurances so they can be sure that you are properly committed to these

targets and, more importantly, you can demonstrate you are actually making

progress.

One of our clients has already committed to getting to Net Zero

by 2030! The political deadline is 2050. But they are of a school of thought that

suggests if we leave it until then nothing would get done and it would be too

late.

How we can help

Net Zero is both a big and intricate subject. The above is just a very brief outline and

there are a range of other tools and standards that we can help you with. The sooner we embrace the Net Zero journey

the more likely we are to avert catastrophic climate change.